Airwallex isn't just another Fintech; it's a global payments powerhouse built in Australia that's solving the biggest headache for international businesses: cross-border banking. By offering easy remote account opening, multi-currency cards, and a Stripe-like payment gateway, it's becoming the go-to alternative for companies fed up with the slow, complex world of traditional banks, especially for those setting up shop in Hong Kong.

The $5.5 Billion Fintech Quietly Solving Global Business's Biggest Nightmare

Ask any entrepreneur setting up a company overseas, especially in a top-tier hub like Hong Kong, what keeps them up at night. It’s not the legal paperwork – that's surprisingly fast. It’s the banking. The soul-crushing, weeks-long (if you're lucky) ordeal of trying to convince a traditional bank to give your perfectly legitimate foreign-owned business an account, often culminating in a mandatory, expensive flight halfway across the world for a 30-minute meeting.

It’s a nightmare that’s killed countless global business ambitions. But a Melbourne-born Fintech, now valued at a cool $5.5 billion USD, has been methodically building the antidote. Airwallex, founded in 2015, isn't just aiming to be cheaper than your bank; it's building a fundamentally different product – a borderless financial infrastructure designed from the ground up for the way businesses actually operate in the 21st century.

And it’s working. From Formula 1 teams like McLaren to major e-commerce players and legions of SMEs, businesses are flocking to Airwallex, not just to save money, but to escape the friction of the old banking world. For international founders, particularly those leveraging efficient structures like Hong Kong companies, it’s becoming less an alternative and more the default operating system.

Beyond Price: The Tech Stack Making Banks Look Ancient

While Fintechs often compete on lower fees, Airwallex's real differentiator, according to Marcus from their Hong Kong partnerships team, is the product itself. It’s a suite of tools designed to handle the messy reality of cross-border commerce.

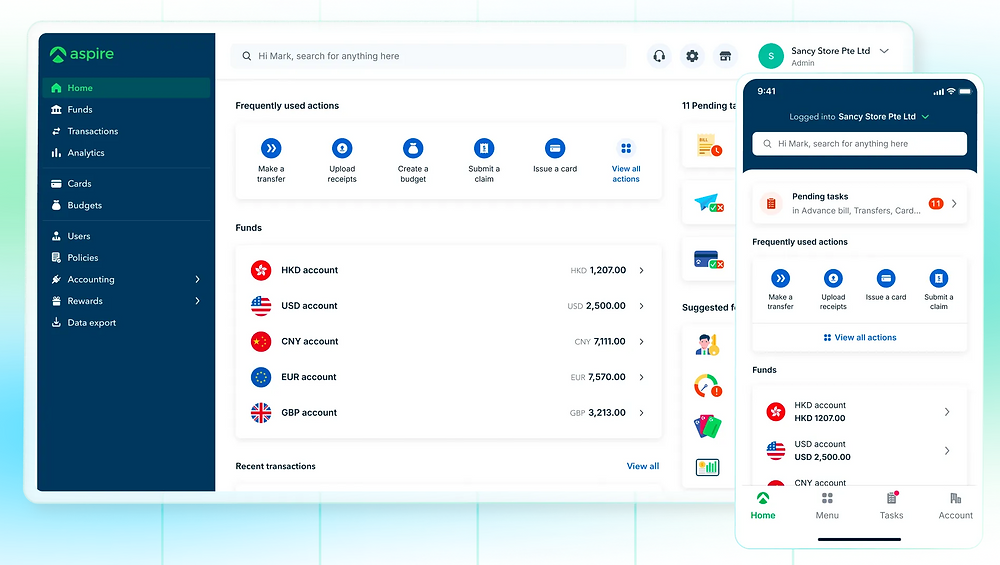

- Global Accounts on Demand: Imagine needing to collect payments in the US or UK. With a traditional bank, that often means setting up separate local entities and bank accounts – a costly, time-consuming nightmare. Airwallex flips the script. "Businesses can access local accounts in 12 different locations with a single registration," Marcus explains. Set up your Airwallex profile, whether linked to your Hong Kong entity or another offshore structure, and you can instantly spin up virtual accounts in major markets like the US, UK, Europe, and Australia to collect local currency like a local business.

- Cards That Speak the World's Currencies: Traditional corporate cards are usually stuck in USD or HKD. Try paying a European supplier in Euros, and you're hit with painful FX conversion fees. Airwallex offers corporate cards (both virtual and physical) that allow direct payments in 10 different currencies. It seems simple, but it's a massive cost-saver for companies with international expenses.

- A Payment Gateway to Rival Stripe: Airwallex isn't just for paying suppliers; it helps you get paid. They offer a full-blown online payment gateway, competing directly with Stripe and PayPal. But crucially, it integrates with a network of over 60 payment methods, including popular local options often missed by the big players. "Think Klarna in Europe, or Afterpay for 'Buy Now, Pay Later'," notes Marcus. Offering these local methods isn't just convenient; it demonstrably boosts conversion rates for online merchants targeting specific regions.

- An Interface That Doesn't Require a PhD: Forget the clunky, decade-old interfaces of traditional bank portals. Airwallex offers a clean, intuitive web dashboard and mobile app designed for ease of use. Everything in one place, accessible from anywhere.

It's this integrated, user-friendly tech stack that’s attracting not just SMEs but also major enterprises. Even other successful Fintechs like Brex use Airwallex's infrastructure for their own white-label solutions.

The Hong Kong Banking Problem Child: Why Fintech is Winning

The rise of Airwallex in Asia is deeply intertwined with the notorious difficulty of opening traditional bank accounts in Hong Kong, especially for foreign-owned companies. For years, corporate service providers helping clients incorporate in Hong Kong faced a critical uncertainty: could they actually get their client banked?

"Traditional banks here make the account opening process tough, particularly for overseas companies," Marcus ( Channel Partnerships Lead at Airwallex ) acknowledges. This isn't just anecdotal; it's a major operational hurdle. Banks demand extensive paperwork, proof of local business substance, and often require directors to fly in for face-to-face meetings – all with no guarantee of approval, and a process that can drag on for months.

This is where the synergy between a service provider like Athenasia and a platform like Airwallex creates a powerful solution. We handle the swift, fully remote incorporation of the Hong Kong company in a matter of days. Then, instead of sending the client into the black hole of traditional banking, we facilitate their application to Airwallex.

"The account opening is remote and online, typically taking around three days," says Marcus. "It removes that huge uncertainty." This streamlined incorporation-plus-banking process allows us, as service providers, to confidently market Hong Kong's advantages without the asterisk about banking difficulties. We can manage the application process, ensuring clear communication and transparency – a stark contrast to the often opaque decision-making of traditional banks.

The Speed Bump: Why Payments Sometimes Get Blocked (and How to Avoid It)

A common misconception is that Fintechs operate with looser rules than traditional banks. The reality, Marcus emphasizes, is the opposite. "Airwallex works with traditional banks in the backend. To maintain those relationships, we need strict compliance and transaction monitoring."

This means payments can get blocked, causing frustration if clients aren't prepared. The two main scenarios are:

- Personal Payments: Airwallex is strictly B2B. Trying to pay individuals for non-business purposes will likely get flagged and blocked.

- New Account Scrutiny: "This is more common with newly opened accounts," Marcus explains. Without an established transaction history, the compliance system might flag the first few significant business payments, especially large ones. Airwallex will then request supporting documents like contracts or invoices to verify the legitimacy of the transaction. Once a pattern is established, these checks become less frequent.

Personal Payments: Airwallex is strictly B2B. Trying to pay individuals for non-business purposes will likely get flagged and blocked.

New Account Scrutiny: "This is more common with newly opened accounts," Marcus explains. Without an established transaction history, the compliance system might flag the first few significant business payments, especially large ones. Airwallex will then request supporting documents like contracts or invoices to verify the legitimacy of the transaction. Once a pattern is established, these checks become less frequent.

The solution? Proactive communication. For large initial transactions, Marcus advises clients (or their service providers acting on their behalf) to send the supporting documents to Airwallex before making the payment. "Leverage the partnership," he suggests. A dedicated support channel through partners like Athenasia can help smooth out these initial bumps. It’s about understanding the rules of the game, not trying to bypass them.

Getting Your Store Online: Merchant Account Hurdles

For e-commerce businesses wanting to use Airwallex's payment gateway, there's another application layer. Not all businesses qualify (high-risk sectors like gift card resellers are often excluded). Airwallex scrutinizes the merchant's website for legitimacy, requiring clear shipping and privacy policies and ensuring reasonable product quality.

Crucially, they look at your track record. "Providing records from previous payment providers, showing low dispute and chargeback rates, really helps," Marcus notes. High refund rates are a red flag, signaling potential customer dissatisfaction or product issues, which can sink an application.

What’s Next? Global Reach and Credit Cards

Airwallex isn't standing still. Their 2025 roadmap includes aggressive expansion. They've recently added support for businesses in Southeast Asian markets like Thailand, Vietnam, and the Philippines. The big news for Hong Kong clients is the planned launch of Visa credit cards with actual credit lines, moving beyond the current debit/prepaid card offering.

Further afield, they're making major inroads into Latin America, having acquired a payments company in Mexico and secured a license in Brazil. The mission remains clear: build a truly global financial network.

But Is It Safe? The Billion-Dollar Trust Question

For businesses used to the perceived solidity of traditional banks, moving significant funds through a relatively young Fintech can feel risky. How safe is money held with Airwallex?

Marcus points to several layers of security and credibility:

- Regulation: Airwallex is fully licensed in every jurisdiction it operates in (e.g., as a Money Service Operator in Hong Kong, regulated by MAS in Singapore).

- Track Record & Partnerships: The company is nearly a decade old and trusted by major global corporations like McLaren, Brex, Casetify, and JD.com. These aren't companies that gamble with their finances.

- Blue-Chip Investors: Airwallex is backed by some of the biggest names in finance and tech, including MasterCard, Tencent, Salesforce, and top-tier VCs. They've raised over $1 billion USD in funding.

While Fintechs lack the government deposit insurance of traditional banks, Airwallex's scale, regulatory standing, and blue-chip backing provide substantial reassurance. It's built for the long haul.

The verdict is increasingly clear. For international businesses, especially those leveraging the strategic advantages of a Hong Kong company, Fintech platforms like Airwallex are no longer just a "Plan B." They are the smarter, faster, and more globally-aligned "Plan A."

By understanding their capabilities and navigating their compliance requirements – often with the help of a knowledgeable service provider – founders can finally bypass the old banking gatekeepers and build truly borderless businesses.